June 17th

Birds flock, the bond market doesn't.

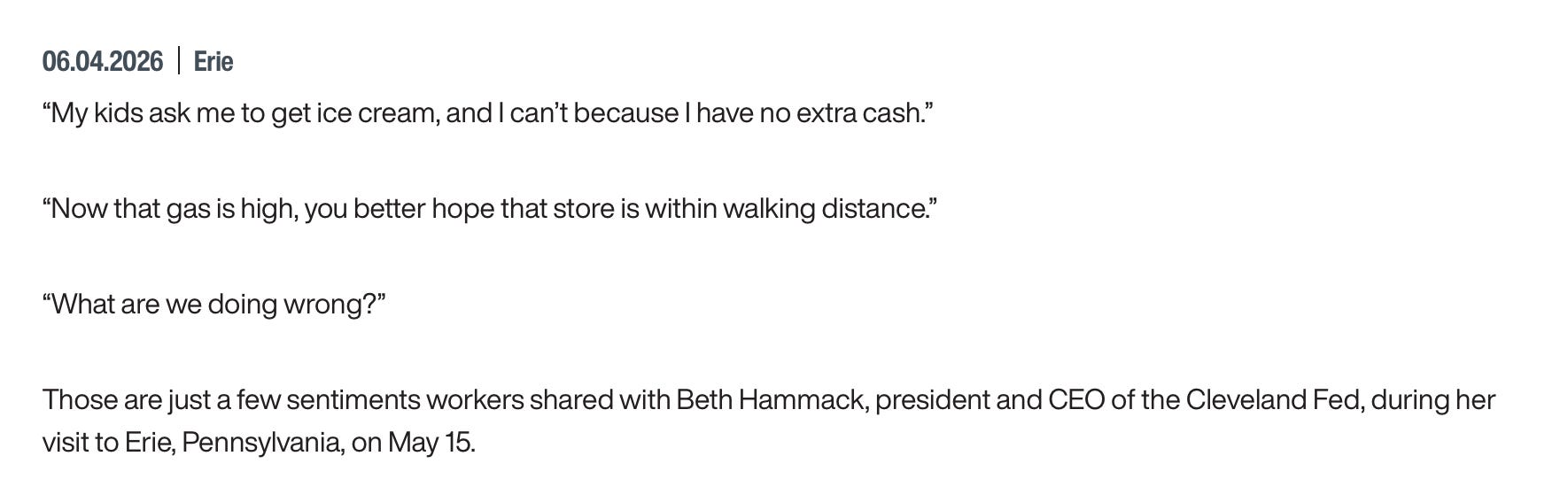

A father in Erie missed all of his son’s travel football games this spring because he couldn’t afford the gas. Hammack relayed the same gas-shock distress Sahm is picking up in the survey data.

The disinflation case is loud, and now politically backed. It is still a bet against the entire front end.

Saying dove, trading hawk — Donnelly’s survey of 467 market participants found that respondents expect a dovish tone from Warsh while being positioned long USD and paid on rates. That is the thesis I set out in April, that Warsh broke the hawk/dove binary, field-tested by accident.

Timiraos’s judgement — that the debate has skipped neutral and is now about a tightening bias by July and when to take back the ‘insurance’ 2025 cuts — is the Fed-whisperer read, and it sits right on top of what the strip prices.

The 17th isn’t just a rate decision. It carries a Summary of Economic Projections and Warsh’s first press conference as chair. The dot plot is still scheduled as part of that SEP — notable in itself, since gutting forward guidance is the reform Warsh has championed. His first dot plot may be among his last.

There is a near-complete consensus on the surface, with the rate decision a formality at roughly 99% priced for a hold. The signal will be entirely in the projections, the tone, and whatever the statement says or stops saying about the balance sheet.

Everyone knows Warsh’s stated agenda — shrink the balance sheet, thin out forward guidance, less ceremony, fewer commitments. And everyone agrees the Committee constrains him. Ethan Harris put it most sharply: the Fed will reform Warsh more than Warsh will reform the Fed. He inherits a committee that split 8–4 in April — the largest dissent bloc since 1992 — and three of the four dissents (Hammack, Kashkari, Logan) were against the dovish easing-bias language, with only Miran dissenting for a cut. Warsh takes Miran’s seat, so the one dove is gone.

The most telling pre-blackout signal came from resident dove Christopher Waller who used a 22 May speech in Frankfurt (on the same day Warsh was sworn in as chair) to perform a near-complete U-turn: he would now drop the easing bias to make a cut no more likely than a hike, and could no longer rule out a hike if inflation doesn’t abate. That’s the speech bond markets reacted to on May 22 when they priced in a 2026 hike.

Reading Friday’s strong jobs print (+172k vs expectations 80-88k), Timiraos judges the internal debate has skipped past whether to go neutral, toward whether to adopt a tightening bias as soon as July and when to claw back 2025’s “insurance” cuts.

And there is a nuance the coverage has mostly treated as a political story rather than an operational one: Powell is staying on as a sitting governor rather than resigning with the chairmanship as his predecessors did — for a period he’s left deliberately open, with his term running to January 2028 — so Warsh chairs a table that still seats the man he replaced. Powell’s presence keeps the board’s composition stable and denies the administration an extra appointment.

The FOMC blackout begins now, so the run of Fed commentary through late May and early June is among the last official words before the building goes quiet, and they skew distinctly hawkish-on-language.

The state of the economy: stable on top, fraying underneath

Before any of the policy reads make sense, you have to see the economy the way the Committee is seeing it, because it’s genuinely awkward.

Start with the labour market, because that’s where the disagreement is sharpest (both in itself and in terms of its implications) and most instructive. On the surface it looks fine, even strong: the May payrolls print that landed on Friday came in at +172k against expectations of 80-88k, with prior months revised up by 93k and wage growth around 0.3%.

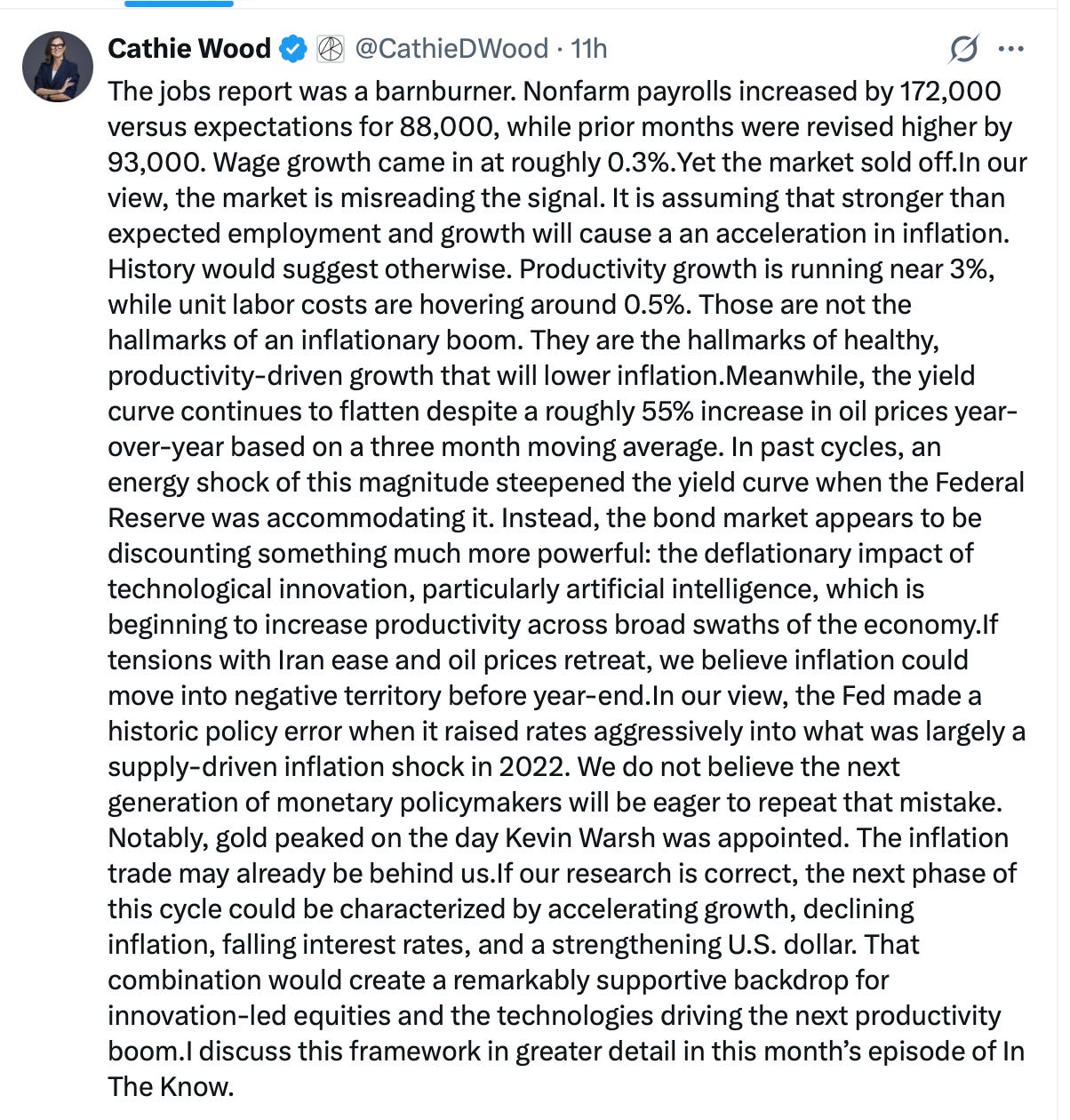

Cathie Wood seized on this to argue the market is misreading economic strength as inflationary when they are instead “hallmarks of healthy, productivity-driven growth that will lower inflation”:

Kevin Hassett, on CNBC, made the same argument, that the jobs strength is a supply-side, productivity boom rather than a Phillips-curve overheating, so the Fed has room to cut and shouldn’t hike at all. He told CNBC the Fed can still cut rates:

"This is a supply side jobs number, which means you can have growth and low inflation. And so this is a kind of story that suggests that the Fed shouldn't hike rates. It shouldn't at all. And it'll have room as it watches the numbers to cut rates."

The disinflation case is loud, and now politically backed. It is still a bet against the entire front end and the view that inflation is structural — a genuine upward shift in the nominal-growth regime. Matthew Klein for instance argues wage growth is feeding the supercore services prices that won’t come down. Kirk Spano argues it’s an energy passthrough that gets worse before it fades. But the sharpest practical point is from Brent Donnelly:

Warsh can lean dovish at the press conference by pointing at his preferred Dallas Fed trimmed-mean measure — and the anchored forwards give him the cover to do it.

But he also shows that trimmed mean is a lagging series, correlating with core PCE at something like 92% when you lag it four months, which means it will be “ripping higher” by the autumn. The dovish cover is real, and it is on a timer. It lasts exactly as long as the forwards stay anchored.

Sahm on the consumer

The consumer is the second pillar, and here Claudia Sahm’s work is the most useful thing in the set. Her point is that consumer sentiment has cratered to record lows, and while an enormous and widening partisan gap now distorts the Michigan survey — to the point where the “all-time low” label is partly an artefact of a 2024 change in survey method — the pessimism is real and it has deepened across both parties, not just the side out of power. What’s driving it isn’t politics; it’s that gasoline is roughly 50% more expensive than it was in late February. That’s the signal worth carrying: the fact that a genuine, bipartisan mood shift is tracking a genuine energy shock — and an energy shock that hits lower-income households first and hardest is a direct threat to the consumption that has been holding the expansion up.

Beth Hammack, the Cleveland Fed president — and one of the three who dissented in April against signalling future cuts — relayed the same gas-shock distress Sahm is picking up in the survey data, down to a father in Erie who had stopped driving to his son’s football games because filling the tank took too much of the budget.

In a speech last week, Hammack came down hard on one side of the box: more worried about persistently elevated inflation than about employment, warning that if the Committee waits for proof inflation has become embedded, the eventual adjustment will be larger and costlier.

“Preventing an inflationary mindset is critical to delivering on our 2 percent objective. Increases in inflation expectations that threaten our goal warrant taking decisive action. For today, it's reasonable to keep rates steady given the uncertainties around the economic outlook. But if recent trends continue, it may soon be appropriate to act.”

Put the three together and you get the box Warsh is in. A consumer whose mood has broken, inflation near 3.8% on an energy shock the Fed can’t touch, and no comfortable place to put the dots. The SEP is going to be an exercise in choosing which risk to disrespect.

What I’m watching into the 17th

The two inflation prints come first and they set the table — CPI on the 10th, PPI on the 11th — and the projections get drafted around them:

A CPI above 3.5% raises the odds of something hawkish creeping into the statement.

The dot plot itself: Donnelly’s survey expects the median to slide from one cut to no change, so a median hike dot would be the genuine shock.

The balance-sheet language, where I’ll be watching for the word “ample” getting downgraded or any RMP framing — one tool referenced is a story, two in one meeting is a regime change.

The 5y5y forward, which is the single line that decides the inflation debate: still anchored means energy passthrough; drifting up means the bond market has called Klein right and the regime has shifted.

The ACM term premium, to confirm whether the long-end selloff stays an issuance story or curdles into a credibility story.

And the press conference, which is the first time anyone hears Warsh speak as chair rather than as nominee — worth remembering that the live hike risk doesn’t sit at this meeting at all but at July, on Timiraos’s reading of the “soon.”

Underneath it, the liquidity backdrop — the SpaceX listing around the 12th, a multi-billion-dollar funding drain landing days before the meeting, into a tape that is already nervous.

Visit MarketStack The Edit · MarketStack Terminal

MarketStack is free today. But if you value my work, you can pledge for a future subscription. MarketStack is an independent, anonymous publication summarising publicly available commentary and views from across financial media. Nothing here constitutes financial advice or a recommendation to buy, sell or hold any security. All views are a synthesis of public information. Past performance is not a guide to future results. This publication is not authorised or regulated by the Financial Conduct Authority. The author writes anonymously in a personal capacity.

What this meta-analysis covers

The piece doing the regime-level thinking: Matthew Klein’s “still inflationary” labour note (The Overshoot) is 14 May.

Everything else clusters mostly into the 72 hours around Friday’s jobs report: 1 June — Claudia Sahm (Stay-At-Home Macro) on consumer sentiment; Peter Conti-Brown (PCB Central) on Warsh and Fed opacity. 2 June — Beth Hammack, Cleveland Fed president, in person at the City Club of Cleveland — a primary source, and one of April’s dissenters. 3 June — Ethan Harris (Ethan on the Economy) on the Project 2025 hires; Kirk Spano on QT and the liquidity risk. 5 June (jobs day) — Brent Donnelly (am/FX) with his Friday wrap and the positioning survey; Nick Timiraos’s thread reading the print, Hammack’s speech, and the White House; Cathie Wood’s response; the BNP Paribas and Hassett lines come through Timiraos. 6 June — Edgerunner on the June risk calendar.

And the primary FOMC and desk voices bracketing the window: Christopher Waller, Board governor, in Frankfurt on 22 May (his hawkish U-turn).