Selling ice, pricing time

AI is not the internet.

Not investment advice

Chips aren’t fibre. Bulls aren’t betting on the frontier. Look closer and it's the opposite. The frontier melts. What matters for the longer term economics isn't the next model or even how cost-efficient the model is (still important), it's whether last year's chips keep earning after they've been bumped off the cutting edge.

Paradoxically, the bulls are betting more on the old technology than the new, not on the ice that's just been cut, but on how long the old blocks last.

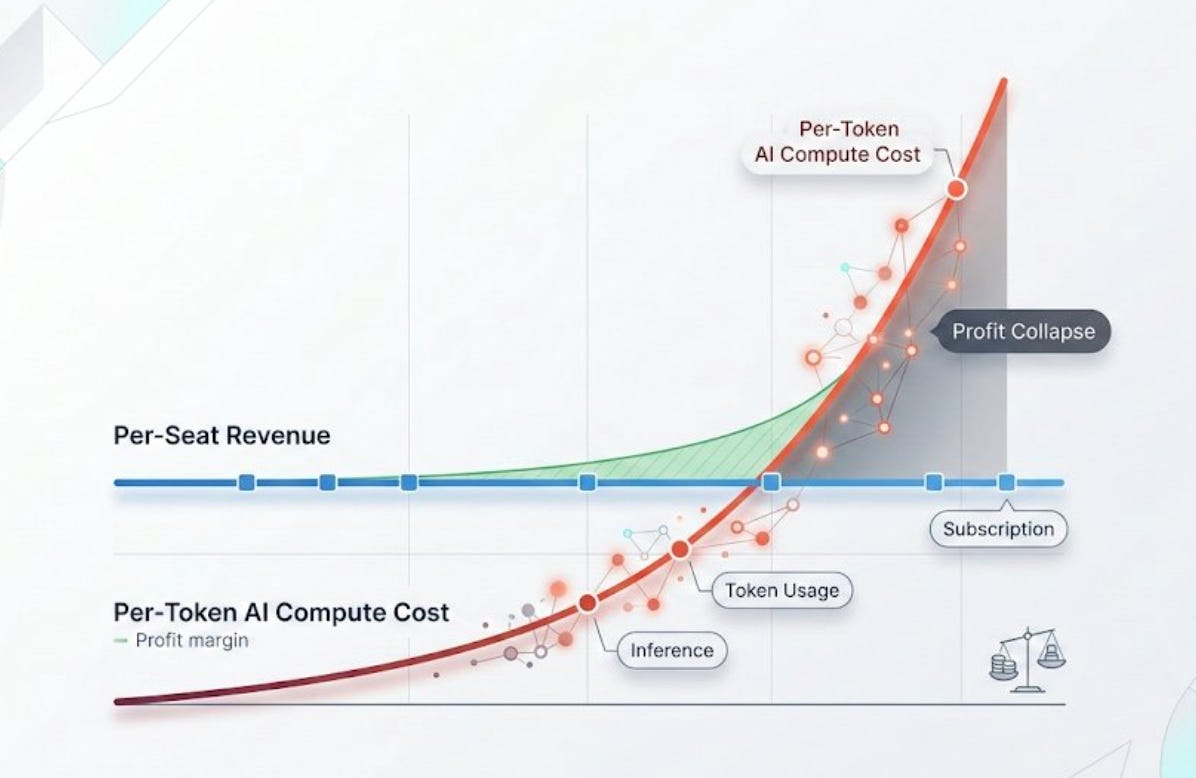

The profit collapse wedge is not the biggest problem

A chart from @hedgiemarkets went viral this week. It shows the SaaS-to-AI business-model margin problem that every AI application company is quietly afraid of: you charge a flat subscription, but your costs scale with how much each user actually uses. Your best customers (power users) then destroy your margin.

Flat subscription revenue » rising per-token cost » profit collapse.

This is the right anxiety for application-layer AI companies. It went viral because it’s true. And it echoes my post last week that the agentic economy’s math is not mathing based on findings from the first system-level characterisation of agent infrastructure costs.

It’s a real problem.

But it’s also a fixable one.

Pricing is already migrating from per-seat to usage-based, and the cost per token has been falling at a rate that makes the curve far less terrifying than it looks. Hold that thought ‘fixable’ because the harder problems are the ones most people aren’t drawing.

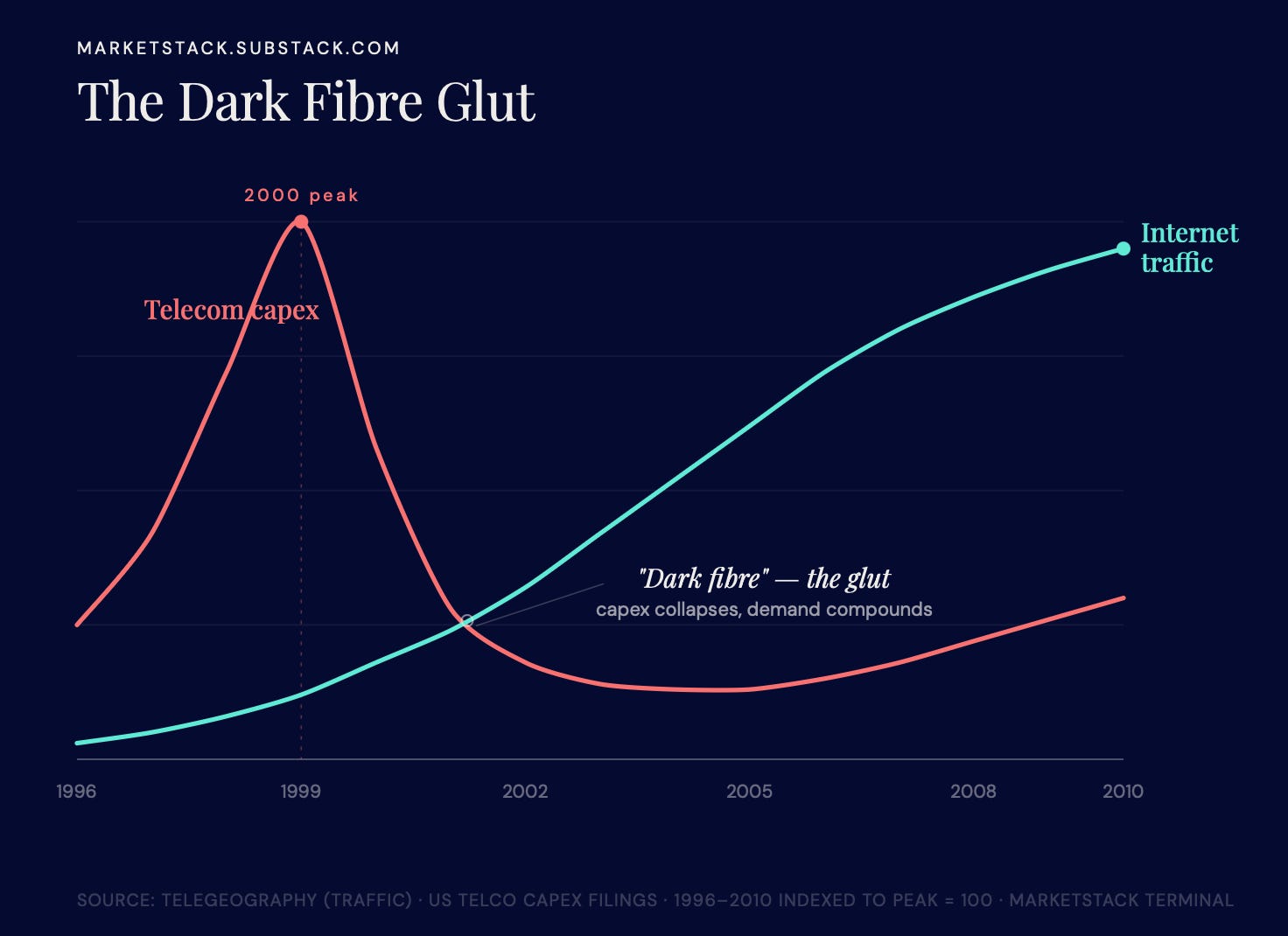

We need to look to Dotcom.

Dotcom does not rhyme

The story you already know: Dotcom looked doomed before the infrastructure got vindicated. Demand wasn’t doubling every 100 days, it was doubling roughly once a year, an order of magnitude slower. The fiction collapsed, the capex halved, and for years most of the fibre sat dark and unused.

But Dotcom’s capex was a bridge to be crossed. Fibre had a long runway to earn back, you could light it in 2008 and it was still earning in 2022, so even slow demand eventually justified it. That’s the under-appreciated nuance in how that played out: the fibre could afford to wait.

Chips are not fibre

Dark fibre had near-zero running cost and didn't decay, so a slow earn-back was survivable. A GPU can't wait. It's competitively stale in ~3 years (contested, see below), so each generation has a narrow window to earn its cost back before the next one renders it obsolete. This strengthens the case for the frame I wrote about NVDA and the UST10Y in Refinancing Faith.

Even if every AI company nails usage-based pricing tomorrow and the per-token margin problem evaporates, the capital sunk into chips that may obsolesce in three years — long before they've earned their cost back — is still there.

This is a much higher bar than fibre ever had to clear. (Almost) everyone is obsessing over a short term survivable margin problem and ignoring the longer term structural one internet infrastructure never had to face.

The obvious rebuttal is the scale of revenue growth, AI usage is exploding at a far greater speed than internet demand, money is pouring in, so where's the problem? Assets can outlive the balance sheets that finance them. But not at perpetual loss. AI infrastructure has a structurally worse version of the unit-economics because it decays. The question is not about demand, it’s does each chip clear its own cost before it's obsolete? The “it’s just dark fibre again” takes miss this entirely.

A chip's cost is paid up front and fixed. The price it can charge falls as cheaper, faster successors arrive — and its competitive life ends when the next generation forces you to replace it. So the margin has to clear the entire cost inside a short window, against a falling price, while you're simultaneously funding the successor. Abundant revenue doesn’t fix that — it’s a profit-per-unit problem, not a top-line one.

The crux of the debate

This is exactly the fight underneath the depreciation controversy: the reported economics look fine only if you spread the chip's cost over the five or six year schedule the hyperscalers use. The bears, Michael Burry foremost, argue the real economic life is closer to three, and on that schedule the per-unit margin may never clear. That gap is the entire fight: it's not a technical accounting footnote but the difference between an industry that's quietly profitable and one that's quietly underwater.

“Understating depreciation by extending useful life of assets artificially boosts earnings — one of the more common frauds of the modern era. Massively ramping capex through purchase of Nvidia chips/servers on a 2-3 yr product cycle should not result in the extension of useful lives of compute equipment. Yet this is exactly what all the hyperscalers have done. By my estimates they will understate depreciation by $176 billion 2026-2028.” — Michael Burry on X.

He went further with company-specific figures: by 2028, Oracle would overstate earnings 26.9%, Meta by 20.8%. He explicitly frames it as a 2–3 year real cycle vs. the 4–6 years booked.

And Amazon already blinked: in February 2025 it completed a new “useful life study” and concluded that the faster pace of AI development meant certain assets would not last six years — a hyperscaler partially conceding Burry’s point in its own filings.

The bull's escape

If old chips keep earning on cheaper inference work after they're bumped from the frontier, the earning life extends past retirement and the economics close. The accounting isn’t fraudulent if the chips genuinely generate revenue for six years, just not at the cutting edge. That is the value cascade.

Paradoxically the bulls are betting more on old technology than they are on the new.

That’s the real crux, the bull case is precisely a bet that the value cascade holds. The depreciation schedule and the cascade aren’t two debates. They’re the same bet, viewed from either end.

This is a falsifiable debate. The cascade either holds or it doesn't, and you can watch it in the rental price of a last-generation chip. While an H100 still rents at a healthy margin, the bulls are winning the argument. When that margin collapses, the bears were right all along.

So what is it saying now?!

The answer isn’t tidy. Resale value says the asset is decaying fast (bear) — used H100 prices have fallen ~85% from peak — but Nvidia is confident enough in H100 demand to raise rental prices ~20% into 2026, saying the old chips are still earning (bull/cascade-holds).

CoreWeave's defense is the single most important counter-fact to the decaying resale value, it defends its depreciation schedules citing five-year customer contracts and 95% resale values for older chips like the A100 and H100. The 85% drop is from the 2023 scarcity peak, CoreWeave's 95% is retention on contracted fleet.

The live empirical test of whether the bull or bear is happening in real time.

Visit MarketStack The Edit · MarketStack Terminal

MarketStack is free today. But if you value my work, you can pledge for a future subscription. MarketStack is an independent, anonymous publication summarising publicly available commentary and views from across financial media. Nothing here constitutes financial advice or a recommendation to buy, sell or hold any security. All views are a synthesis of public information. Past performance is not a guide to future results. This publication is not authorised or regulated by the Financial Conduct Authority. The author writes anonymously in a personal capacity.