The impossible maths of the impossible maths

Confidence is a business model.

Who gets paid to say “dunno”?

There’s another reductive argument on X about a reductive chart. This one’s on a chart from an FT opinion post.

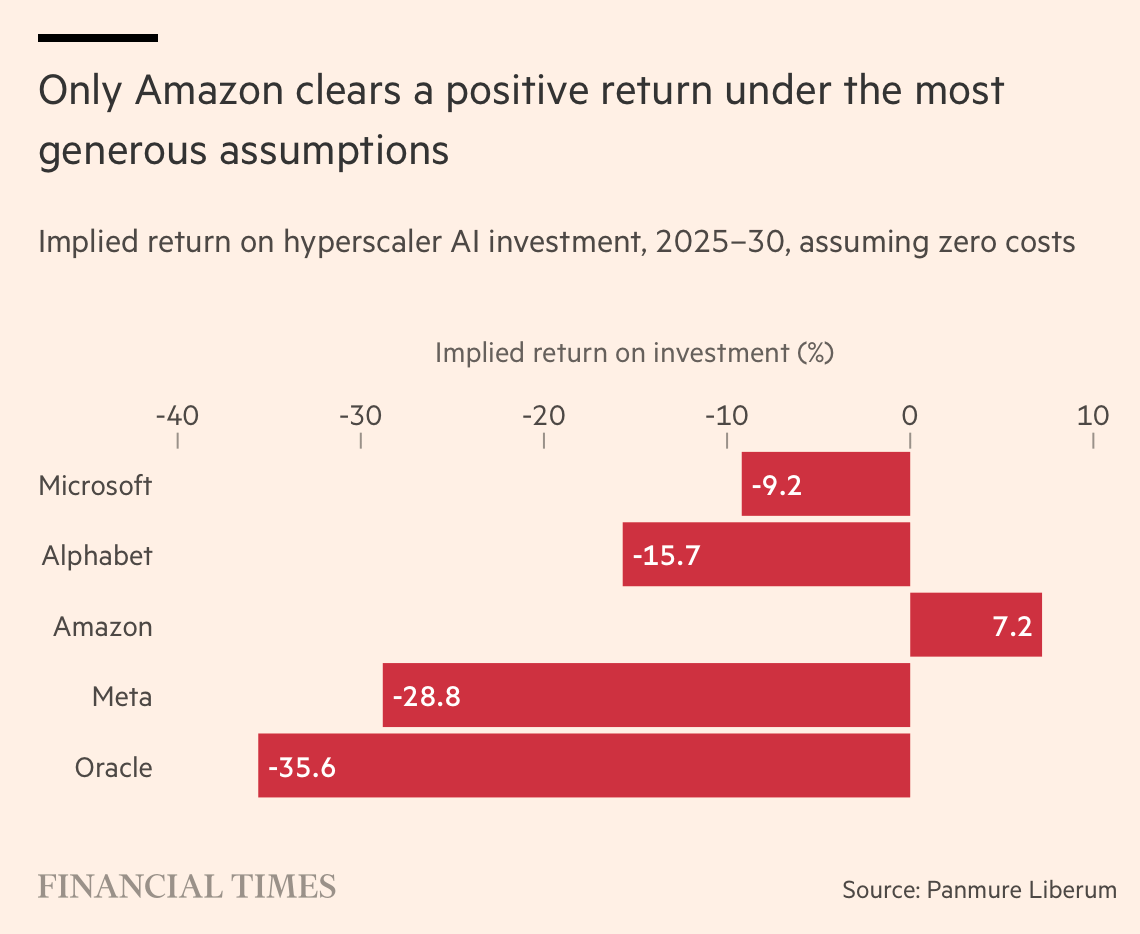

‘The impossible maths of the AI boom’ presents the negative return on hyperscaler capex over an (arbitrary?) 5 year period (in all bar Amazon) as a sort of arithmetically-doomed destiny.

Whilst I share the anxious scepticism on (completely different) numbers, this is a flawed and reductive frame.

Five-year capex ROI is not the arbiter of destiny

Whilst the basic observation that capex is growing faster than revenue is a real tension, it still does not guarantee impossible math. ROI on a multi-decade asset can't be judged over a five-year window when you're front-loading capex. Data centres generate revenue for years beyond 2030, so comparing 2025–2030 capex against 2025–2030 incremental revenue all but guarantees a negative number for a capital-intensive buildout in its investment phase.

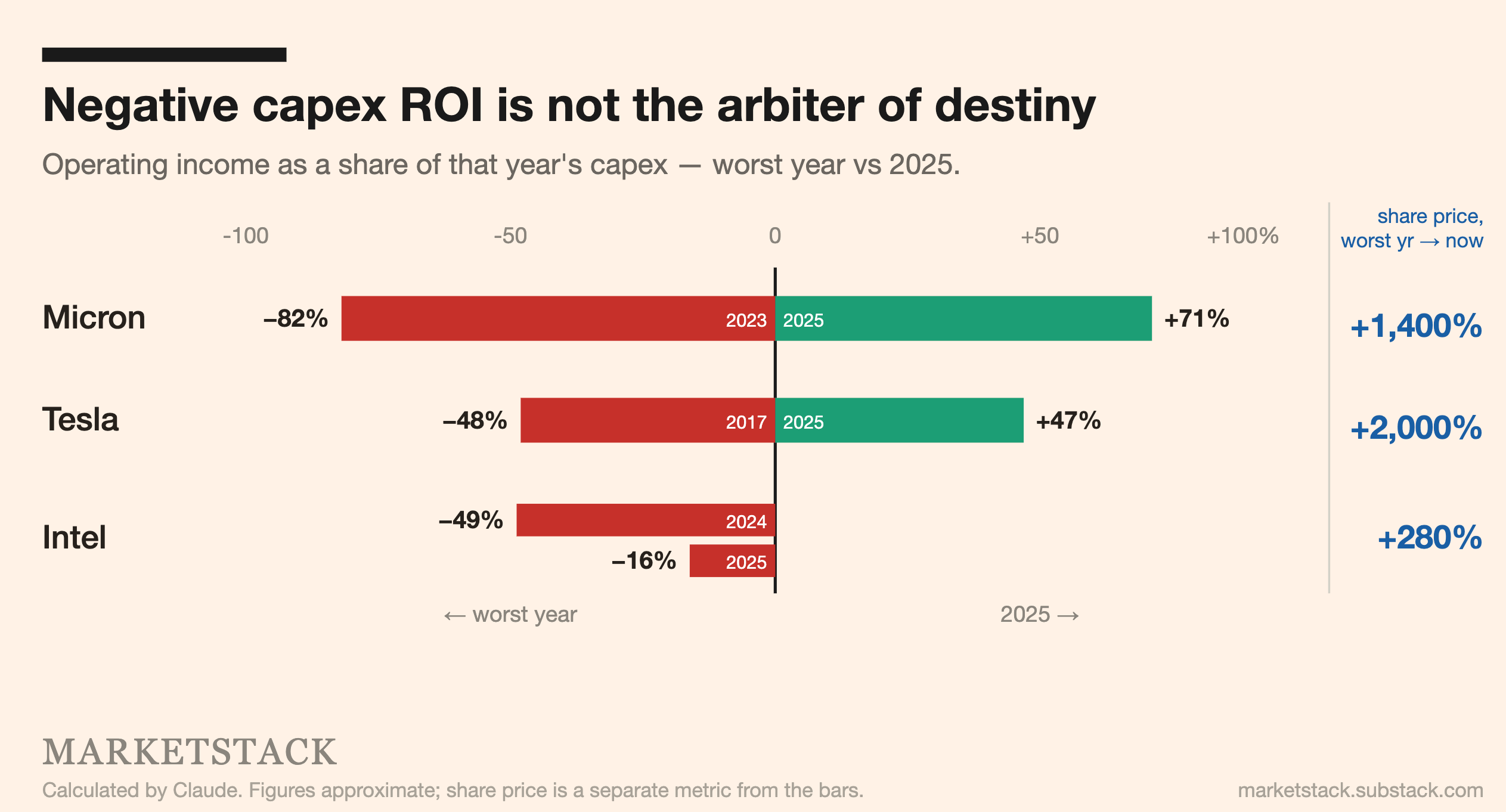

To further demonstrate this point, consider the worst year of these three companies in terms of operating income as a percentage of that year’s capex compared to the same metric in 2025. Using Claude calculations:

Micron swung from −82% in 2023 to +71% in 2025

Tesla from −48% in 2017 to +47% in 2025

and Intel improved from −49% in 2024 to a still-negative −16% in 2025.

Despite those ugly trough years, the return on capex grew substantially whilst the share price ran up from the worst-year low to now — +1,400% for Micron, +2,000% for Tesla, +280% for Intel.

Yes this is a deliberate curation of turnarounds and yes you can find tonnes of examples where the opposite is true but that’s my point. Capex ROI, let alone projected capex ROI (see my next point), is not the determinant of destiny.

Do note, Tesla’s “worst year” is 2017 while the others use much more recent troughs, so the share-price comparisons aren’t measured over a consistent window. The footnote already notes the figures are approximate and that share price is a separate metric.

Uncertainty has no arithmetic

Even if we accept (which I don’t) five years as the period after which positive capex ROI arbitrates hyperscaler returns (which it doesn’t), revenue assumptions are close to futile right now because the price of tokens and their unit economics (independent of price, i.e. useful life) are not only unknown but widely contested and changing in real time. Run unknown inputs through arithmetic and you don’t get knowledge, you get false precision that looks like it. A definite negative (impossible math) is no more honest than a definite positive.

In that sense, presenting zero-cost assumptions as ‘heroic’ and ‘generous’ has the effect of propping up the frame that the math is impossible, obscuring the more honest frame that the math is unknown.

Hyperscalers are pricing that unknown, committing trillions against demand and margins nobody can yet see in full. That’s the risk they’re visibly taking. And, whether they know it or not, it’s the same bet investors are taking, not whether capex return is positive in year five.

See also the complexity useful life adds to the arithmetic in my piece ‘Selling ice, pricing time’.

It gets worse on X

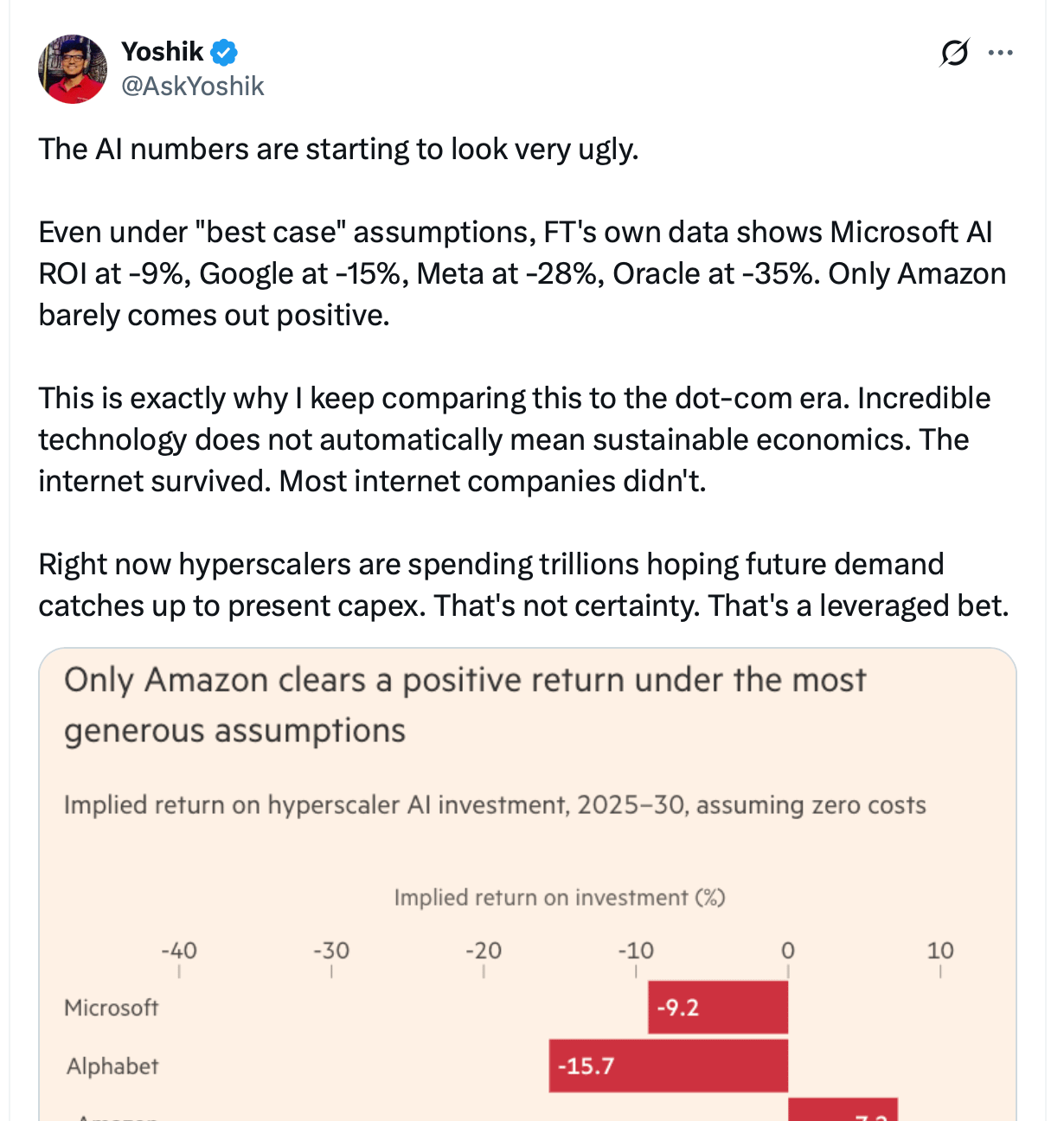

An X post about the FT article that is currently going viral conflates “demand won’t catch up to capex” (not what the FT post said) with “the economics don’t work” (what the FT post said but for reasons I have contested above). He also extrapolates the ‘AI numbers are ugly’ frame into a vindication for the dot-com comparison (eye roll).

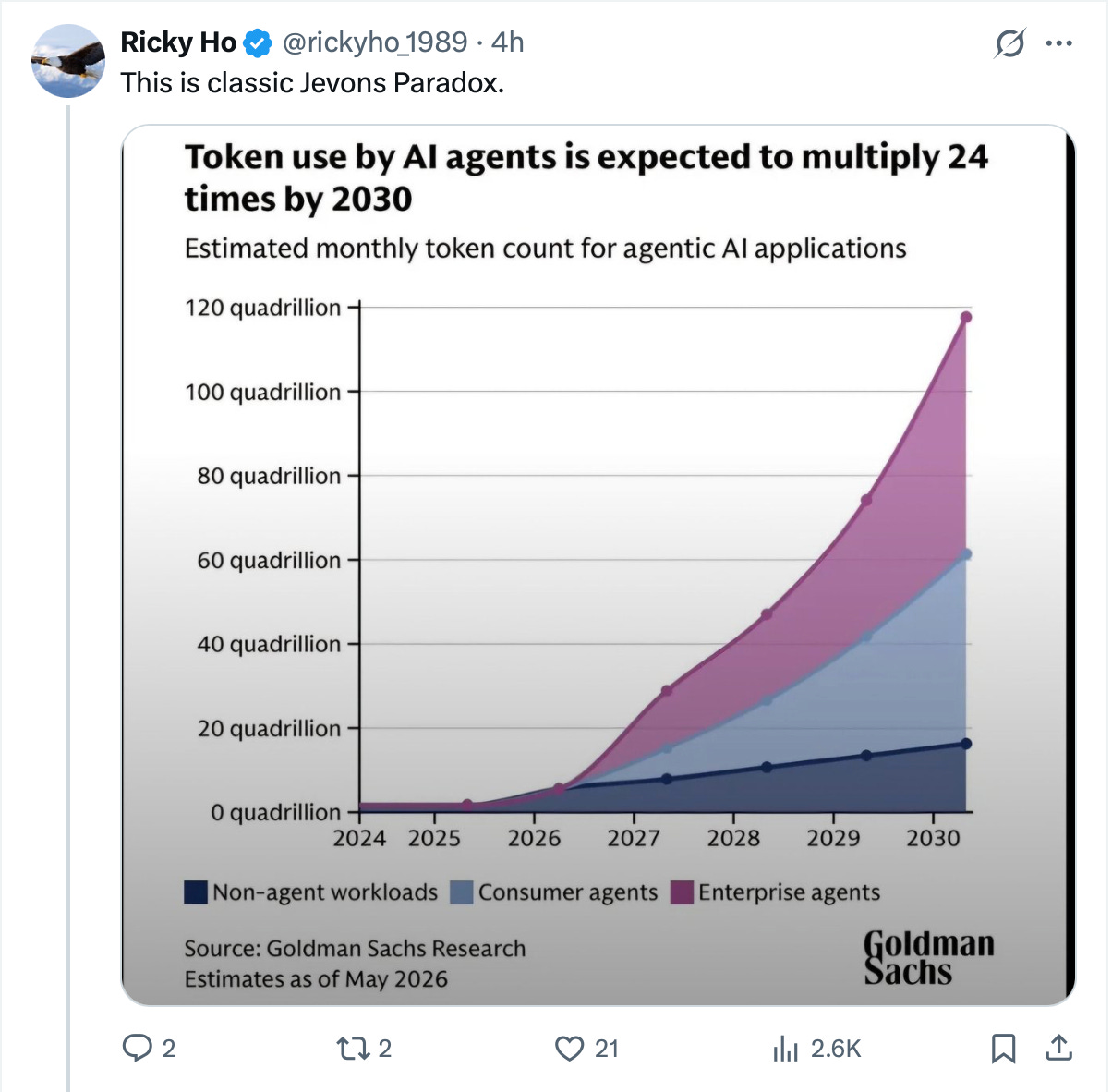

The mis-frame invited a particularly futile rebuttal — Jevons’ paradox, which you’ve probably seen at least 5000 times. But the FT chart never claimed demand won’t show up, it claimed demand showing up at consensus pace won’t cover the capex. To be fair to Ricky Ho, it was a fair rebuttal to Yoshik’s misinterpretation of the FT that hyperscalers are ‘hoping future demand catches up to capex’ but it further reduces the debate to explosive token demand vs unsustainable hyperscaler capex ROI.

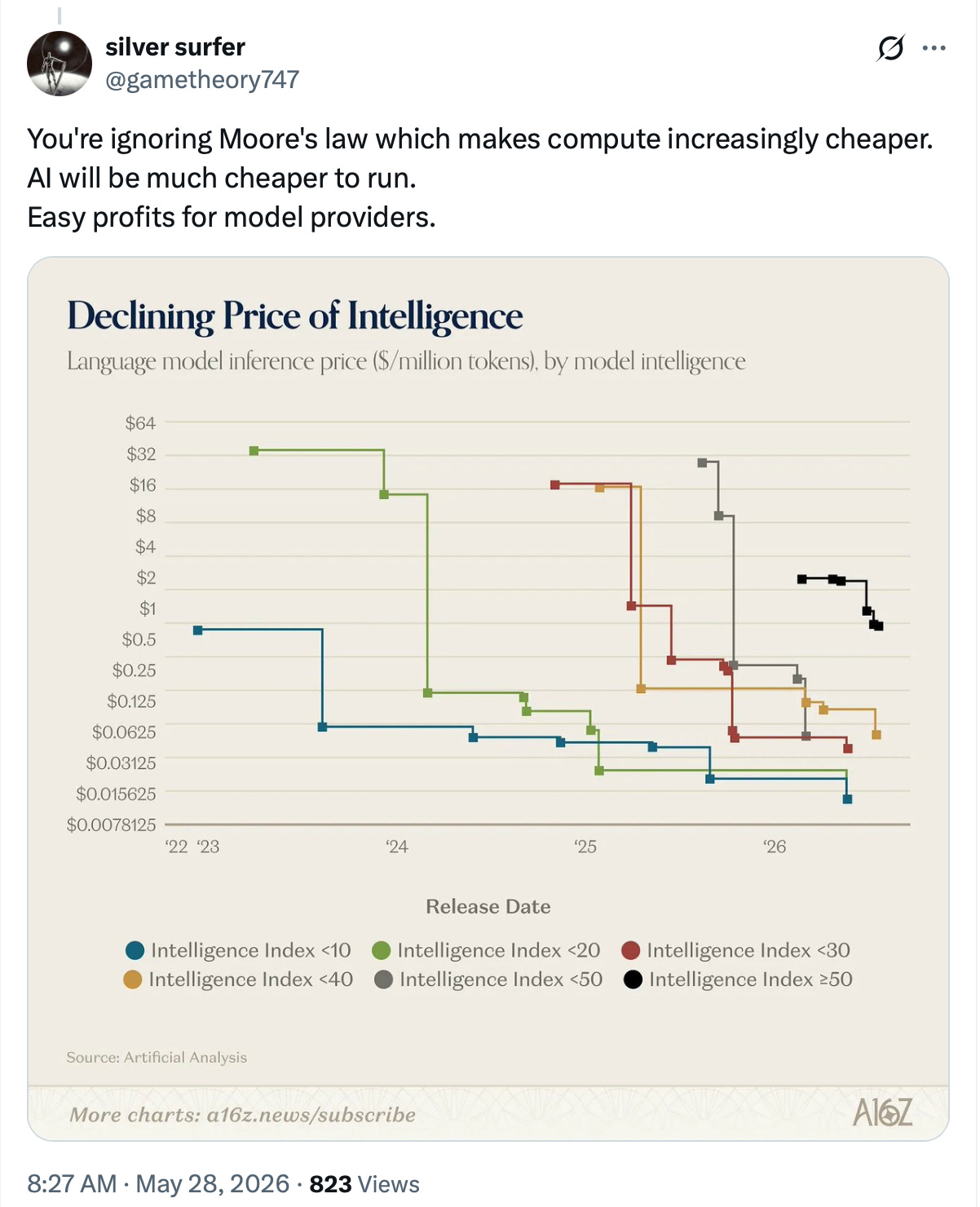

Another commenter shares the viral chart on the collapse of the price of LLM inference. His logic seems to run: cheap compute = easy profits.

But the extent to which cheaper compute passes through to profits ignores how aggressively competitive LLM providers are (commoditisation, price wars, savings competed away) and depends on a lot we don't yet know.

In the meantime an industry gets paid to sound like it does and commentators pick the axis that flatters their priors. The honest chart would plot capex, token demand, and the falling price of inference, and admit nobody knows where the lines cross.

Visit MarketStack The Edit · MarketStack Terminal

MarketStack is free today. But if you value my work, you can pledge for a future subscription. MarketStack is an independent, anonymous publication summarising publicly available commentary and views from across financial media. Nothing here constitutes financial advice or a recommendation to buy, sell or hold any security. All views are a synthesis of public information. Past performance is not a guide to future results. This publication is not authorised or regulated by the Financial Conduct Authority. The author writes anonymously in a personal capacity.

Sorry for the late reply, but I am travelling and your note was long and I found it a bit confusing to go through.

In any case, I would make two points on your rebuttal to my FT article and leave the discussion on the X posts etc. aside, since this is not the point that I was making anyway.

As far as I can see, your two critiques of my FT post are that (i) data centres have a much longer life than five years, so the five-year IRR I am using is too short and hence too low, and (ii) that nobody knows anything about future revenues because the uncertainty is so high, so using the consensus forecasts I have used makes no sense.

I think your critique already fails on point (i). You say that data centres create revenue for years and decades, but that makes the fundamental mistake of looking at a data centre as a building, while in reality it is a computer the size of a building. About 40% of the costs of a data centre are the GPUs (or TPUs, Trainiums, etc.). Another 40% of the cost are the racks, including memory chips, cabling, etc. 20% or less of the cost of a data centre is the building and its cooling system.

The building lasts for decades, the cooling system probably for a decade, but the hardware lasts for less than five years. Companies commonly depreciate IT hardware linearly over five years. The depreciation schedule for Nvidia chips is typically three years, but many companies are now shifting to four or five years (which in itself is a damning indictment). Fact is that Nvidia launches a new generation of GPU every 18 to 24 months, which means that after two years, the GPUs are already outdated and essentially worthless for training and inference tasks on the most advanced LLMs.

Bottom line is that while after five years, the data centre still stands and looks pretty much the same as on day one, 80% of its cost have been written off and 100% of its contents have been replace and are completely replaced by new capex. One could build a complicated model with different depreciation factors, but fact is that 40% of the initial capex (the GPU) has a useful life of about three years, another 40% has a useful life of five years and 20% has a useful life of more than five years. For simplicity, I used a five year useful life for the whole thing.

On point (ii) I readily concede that there is huge uncertainty about the future revenues of data centres. But that uncertainty goes both ways, not just in the direction of higher revenues, and - most importantly - this does not mean that we abandon all analytical approaches and try to price hype. Your subtitle 'Confidence is a business model' is, with all due respect, absolute bs. Confidence and hype are not a business model. Financial markets trade in hype for some time, but in the long run it is all about hard numbers, not hope and fear. Hope and fear is what create bubbles, and these bubbles eventually collapse and that's when people lose a lot of money. Or to paraphrase the eminent 20th century philosopher Jeffrey Lebowski: If you don't have numbers, then that's just your opinion, man.

In any case, my main point in using consensus analyst estimates is that this a is what we have to assume is what is priced in the share price of these companies. And if there is an internal contradiction in these estimates, then the share price of these companies is wrong. In the FT article, I showed that there is a massive internal contradiction in the consensus estimates, so the share price is wrong.

If the share price is wrong, it can be resolved in either of two ways. Either there are more revenues in the future than consensus expects or the capex will be unprofitable and either a waste of money or never deployed in the first place.

As for the revenue opportunity, I calculate that the hyperscalers need to make an additional $2tn to $5tn in revenue by 2030. That is up from $1.5tn in 2025 or a tripling to quadrupling of their revenue base in five years. It's not impossible, but as close to impossible as I have ever seen in a megacap company that already has a global revenue base.

So, I am left with the conclusion that the capex will either never be made or it will be an exercise in massive shareholder value destruction.

One final point. If the future revenues of these hyperscalers are so uncertain, they should also trade at a significantly higher risk premium to reflect that uncertainty. That would devalue their shares even more, which is an argument that I have so far ignored as well.